Experts tell you: when the credit record is bad, how to buy a house?(1)

Credit history is a key indicator of applying for a loan, but many people have this concern about how to get a loan if it has a bad credit history.

A credit score is a decisive factor in determining whether you are eligible to apply for a loan. "Theoretically, the higher the rating, the less risk you face," says Staci Titsworth, regional manager at PNC Mortgage in Pittsburgh, Pennsylvania.

In fact, the average American household owes $15,000 in credit card debt. Under such a premise, many people will be wondering: in the credit history of poor, can be loaned to buy a house? Yes, but if you want the home purchase process to go well, from now on, you'll need to address the economic problems in your credit report. Here, we share expert answers to the concerns of many lenders, including what exactly is a credit report and how to improve your credit score to prepare for a home purchase.

What is a credit score?

It is customary for mortgage lenders to check your credit score, which is calculated based on the information on your credit report. There are five factors that affect the scoring, each with different proportions: 35% of repayment records, 30% of credit lines utilization of arrears, 15% of credit history, 10% of credit structure, 10% new credit, and 10% of new credit. Let's look at these factors one by one.

Repayment records

You should make repayments on time, because a single late payment can have a significant impact on your credit score. For example, according to Equifax, a U.S. credit agency, a consumer who has never missed a credit score of 780 points (850 out of 10) before, and whose credit score is reduced by 90 to 110 points if a 30-day default is delayed.

Credit utilization (debit-to-credit utilization ratio)

That is, divide the amount of arrears accumulated on your credit card by the amount of credit in the total account. Credit experts recommend keeping this ratio at around 30%. If you overdraft your credit card every month, it will damage your credit score.

Length of credit history

The longer your credit history lasts, the higher your credit score. Credit expert Hard Bill Billkopf says credit agencies look at the length of time you opened your earliest and most recent accounts (e.g., 2 years and 3 months) and the average length of time you opened for all accounts. Therefore, you should ensure that all accounts are enabled, even if the account balance is zero.

Credit Mix

Holding different types of credit accounts, such as credit cards, retail accounts, installment loans, car loans and mortgages, will help boost your credit score (the last one is what you're about to apply for).

New credit

Each time you apply for a new credit account, your credit receives a "hard inquiry" that results in a reduction in your credit score (usually 5 points). Therefore, Hardekopf recommends that you try not to open multiple credit accounts at the same time. Doing so will shorten the average opening time of your credit account and damage your credit history.

Advice: There will be no clear credit score in the credit report. However, your credit card company is likely to give you a free rating, or you can contact a non-profit credit advisor to check your score.

What is the ideal credit score?

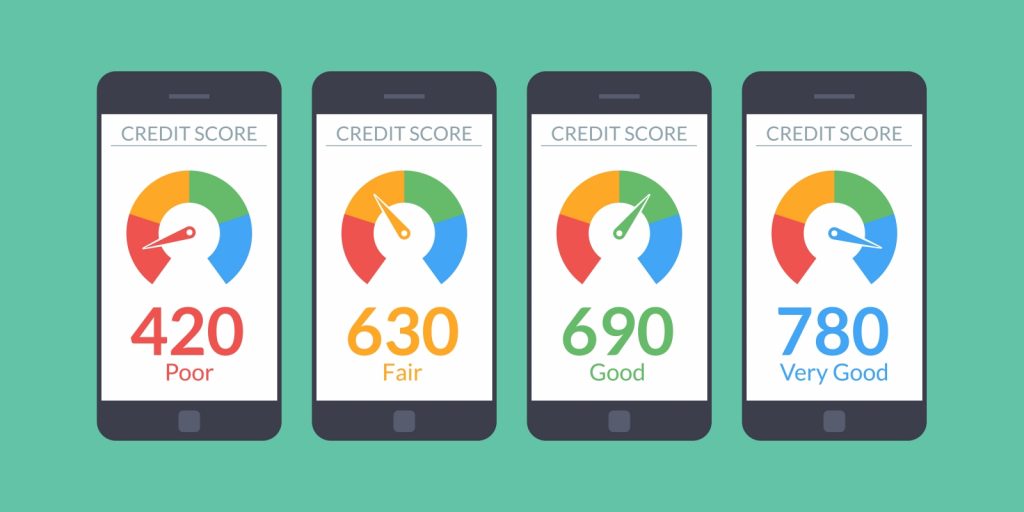

According to Fair Isaac Corporation, the founder of the extensive FICO credit score, the perfect credit score is 850, but only 0.5% of consumers can achieve it. Chris Hauber, a mortgage sponsor at Hallmark Home Mortgage, a mortgage company in Denver, Colorado, says that as long as your credit score exceeds 740, you'll meet the ideal mortgage lender's standards and enjoy the best rates.

If your credit score is just over 700, you'll still be able to enjoy a better rate. For regular loans, Hauber says, most lenders will require you to have a credit score of at least 620. Applicants must have a credit score of at least 660 points to qualify for a relatively favorable interest rate and can apply for a loan without additional requirements.

If I don't have a credit history, can I apply for a loan?

Ideally, you should open a credit card account at the age of 20, or, as a teenager, build your credit by becoming an authorized user of your parent's credit card. (Remember, the length of your credit history has a significant impact on how your credit score is calculated.) If you don't have a credit history, you can also qualify for a mortgage and start building a credit history. "Many lenders look at your monthly payment obligations, and these obligations don't necessarily appear on your credit report," Titsworth said. "Experts point out that if you can pay back your car loan on time and pay the rent, it will also help. Often, these habits reflect whether you are a responsible credit user.

Bad credit is worse than no credit?

In maintaining credit, some leaks are inevitable. Maybe, occasionally, you forget to pay back the minimum repayment limit on your credit card bill, or you recently found an error in your credit report when you discussed a loan option with a mortgage lender. In either case, you can take steps to remedy it. "A bad credit history can be reversed," Titsworth points out. "

In addition, there are loan programs designed to help home buyers with moderate ratings. Federal Housing Administration (FHA) loans have the lowest credit score requirement, at 580, with a down payment of 3.5%. Loans from the U.S. Department of Veterans Affairs can keep veterans' home purchases as low as 0% without having to pay private mortgage insurance.