Financial report anatomy | veteran empire Microsoft is still strong

This earnings season is particularly difficult to bet on. This is mainly reflected in the obvious differentiation of the giants, which is basically a song of ice and fire, and there are too many factors to consider. Facebook's first financial report in 2 years fell short of expectations (except for 20Q1, which was affected by the epidemic), and Snap's lowered revenue expectations have made the market believe that the overall performance of advertising will be relatively poor. Yesterday, Google’s financial report was relatively strong, with revenue and profit double beat, but a significant slowdown in growth can also be seen.

When the market was under pressure from inflation, supply chain, and resumption of work, Tesla handed over a fierce financial report. He just dragged the Nasdaq upwards and refused. And yesterday after the market, Microsoft also handed over a dazzling performance report, which once again formed some support for the Nasdaq. Let’s take a look.

Microsoft's new quarter earnings report is generally strong in terms of revenue and profit double beat. Revenue of 45.3 billion US dollars, an increase of 22% year-on-year, higher than market expectations of 43.93 billion US dollars; EPS 2.71 US dollars, significantly higher than the expected 2.07 US dollars; net profit of 20.5 billion US dollars, an increase of 48% year-on-year.

Breaking down, revenue from products (systems, office software, etc.) was US$16.6 billion, a year-on-year increase of 5.2%; revenue from services (cloud computing, etc.) was US$28.7 billion, a year-on-year increase of 34%. Product gross profit margin was 77.2%, which was basically the same as the same period last year; service gross profit margin was 65.7%, which was basically the same as 65.3% in the same period last year.

From the perspective of this revenue structure, the obvious trend is that Microsoft’s growth is mainly driven by services such as cloud computing (Amazon is also similar). Although the profit margin of this track is not as high as that of traditional products, the slope is long and thick-the future is In the data age, the industrial Internet is still expanding at a high speed, and the cloud is the foundation of all this. Although Microsoft Azure is not as large and comprehensive as Amazon in terms of cloud services, it has the natural advantage of synergizing with Office 365 and other office software, and Long Er's position is still very stable.

Further split the growth of different product lines:

The highest growth is Linkendln, Azure, Dynamics365, which increased by 42%, 50% and 48% respectively. Looking back at Microsoft's operating data in recent years, Smart Cloud has always been the fastest-growing sector, with a growth rate of 31% this quarter, setting a new high in the past three years. At the same time, rapid expansion has made Smart Cloud the top of Microsoft's three major business units for three consecutive quarters.

Azure has a very high position within Microsoft, and it is also the most promising business in the market (similar to the logic of Amazon aws). Previously, analyst Canalys released a report showing that the global cloud computing market in the first quarter of this year increased by 35% year-on-year to 42 billion US dollars, of which Microsoft Azure had a market share of 19%, second only to Amazon (AWS) with 32%. , Google ranks third with a market share of 7%. The report also stated that Microsoft plans to build 50-100 new data centers around the world every year. In the foreseeable future, the overall cloud computing industry is still expected to maintain a high double-digit growth trend.

In addition, the growth of Office 365 is also good, with 23%. This growth structure still has a trend to maintain, which means that Microsoft's ecosystem is very solid and is still expanding steadily and rapidly. It’s also worth noting that search and news advertising also experienced a high growth of 40% year-on-year, which is also a good sign.

Next, look at the cost side. Research and development costs are US$5.6 billion, accounting for 12.4% of revenue, which is a decrease from 13.25% in the same period last year. However, the absolute value is still very large, with a year-on-year increase of 14.3%, which is a relatively stable level. Marketing costs are US$4.5 billion, accounting for 10% of revenue, which is down from 11.4% last year, which means that the marginal revenue of marketing has increased. This is a very good signal.

In the end, the overall management cost is US$1.29 billion, accounting for 2.8% of revenue, which is a very low level (on the one hand, because of Microsoft’s asset-light model, the jobs are high-end, and the per capita value created is high; on the other hand, due to the scale effect), last year Compared with 3% in the same period, there is still a slight decrease. On the whole, the three fees are in good condition, which brings a terrifying 44.7% high operating profit margin.

On the whole, Microsoft's ecological barriers are very high, and there are still strong growth expectations in the future, and the core focus is still on the cloud service business represented by Azure. In addition, Microsoft has launched a new Surface PC and said it is acquiring security startups CloudKnox and RiskIQ. The company has also hired Charlie Bell, a former executive of Amazon’s cloud computing business, to engage in cybersecurity work and promised to invest in security research and development. More funding. The business of the network security track is getting higher and higher, and there have been many data security incidents (Facebook, Amazon...) in the past few months. In the future, the state and capital investment in this area will continue to increase. Trends, related concepts and individual stock analysis can be found in our previous article analysis, which deserves great attention.

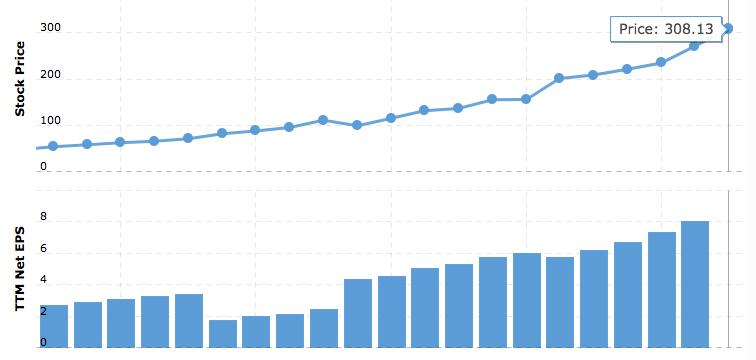

The current valuation of 38x is not cheap and belongs to a higher position within 5 years. However, strong growth in cloud services and steady growth in other businesses can deliver performance, gradually digesting this valuation level. In the short term, the stroke value may not be high, but in the medium and long term, Microsoft is still the preferred choice worthy of configuration.