Nike has entered a rapid growth cycle, and the stock price still has more room to rise in the market outlook?

In the past few months, the stock price of sportswear giant Nike (NYSE:NKE) has seen an amazing rebound.

There are signs that the Oregon-based company is establishing a new financial model that will continue to promote the company's long-term sustainable growth. Driven by soaring sales, the company's stock price rose by about 25% over the same period.

Behind this boom is the company's record quarterly sales data. This is the first time in the company's 50-year history that revenue has exceeded $12 billion. And this sales expansion data from the post-epidemic era also sends a strong signal to investors, that is to say, this manufacturer of "Air Force One", Jordan, and Converse sneakers is entering another rapid growth. This also makes the company’s stock price extra attractive.

However, after such growth, investors will inevitably ask questions. How long will this rebound last? Has Nike's stock price reached the overbought range? Before answering these questions, we need to understand some of the influencing factors currently facing Nike.

Factor one: suppressed demand is recovering

During the epidemic, people were forced to stay at home, sports events were cancelled, and Nike's sales were inevitably affected. In the quarter ending May 2020, its performance fell by approximately 40% from the pre-epidemic USD 10 billion.

However, as the US economy began to restart this spring, Nike’s sales began to rebound rapidly, driven by pent-up demand and consumption power. In the period ending May 31, global sales almost doubled due to a surge in direct shipments to consumers by more than 70%.

Nike's performance in China is also better than some investors had previously worried about. After sensitive political events, the company's sales in Greater China still increased by 17% in the last quarter, reaching US$1.9 billion.

In addition, Nike predicts that the company's sales will also experience double-digit growth for the current fiscal year ending in May next year. Executives expect that with the response of consumer interest, growth in the first half of this year will be even faster. The company’s CEO John Donahoe said, “Nike’s strong performance this quarter and the entire fiscal year proves Nike’s unique competitive advantage and the deep connection between the brand and consumers around the world.”

Factor 2: Digital sales layout, remarkable results

In addition to the short-term influence of the consumption recovery in the post-epidemic period, there are other catalysts that have boosted the bullish sentiment for Nike's future growth.

The global health crisis has accelerated Nike’s transition to e-tailing, creating a direct-to-consumer business model that is not only efficient, but also conducive to improving profit margins. In the past few quarters, Nike’s online sales have soared by more than 80%, exceeding the company’s revenue target in this area, accounting for 30% of sales in China.

And this windfall is not just luck. Just before the outbreak, Nike handed over control to John Donahoe. He used to be an executive of eBay and took over as CEO of Nike on January 13, 2020. , And quickly opened Nike’s electronic sales strategy through the company’s own website and stores.

After Nike launched the Amazon platform in 2019, he reduced the number of wholesale outlets that can sell the company's products. In addition, Nike has invested heavily in improving customers' digital experience, improving its apps and their sports guidance.

In the first few months of the outbreak, Nike closed stores on the one hand and accelerated the process of digital sales on the other hand to attract more consumers who could not go out.

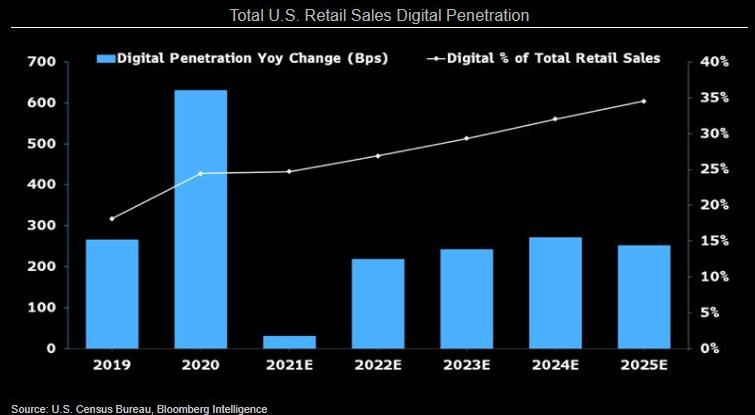

Media analysis shows that the new crown epidemic has accelerated the use of e-commerce platforms by shoppers, thereby changing the retail landscape in the United States. The company predicts that by 2025, the proportion of online shopping in total retail sales will rise from 14% in 2019 to 35%.

In the latest forecast data, Nike predicts that by 2025, its online sales will account for about 60% of China's sales, which is higher than the current 40%.

Factor 3: Wall Street analysts are still optimistic about Nike

Combining the above-mentioned series of forecasts, and as Nike shifts to a lower-cost online sales model, its profit margins have increased significantly. Analysts are optimistic about the athletic footwear and apparel giant’s share price momentum, even after this year’s strong rise. .

Of the 34 analysts surveyed, 29 analysts gave a rating of "outperform" and predicted that the stock's share price would rise by another 8% in the next 12 months. Among them, Oppenheimer’s analysts raised Nike’s target price from US$150 to US$195 last week. They are optimistic that the stock has more room for upside. Analysts believe that “the market underestimates the number-driven Nike business model. Long-term earnings per share will be significantly enhanced."

In addition, Jefferies analyst Randal Konik also wrote in the research report that Nike is one of the best brands in the world. The global consumer base is very strong. The company is further strengthening its connection with consumers through technology. The analyst also gave the company a "Strong Buy" rating.

Nike executives told investors last month that “Nike’s revenue is expected to grow by more than 10% in the fiscal year beginning in June, to more than $50 billion. In the fiscal year that just ended, the company’s revenue increased by 19%.” They also expect that profit margins will expand as the company sells more products directly to consumers.

Factor 4: Greater dividend attractiveness

Due to the potential for additional capital gains, Nike is also the main focus of long-term fixed income investors. Currently, the stock’s quarterly dividend is $0.275 per share, and the annual dividend rate is 1%. Compared with higher-yielding stocks in the market, this yield is obviously not attractive. However, analyzing stocks based solely on earnings is not a good way.

The best dividend stocks are those that regularly increase their dividends. In this regard, Nike has done a good job-the company has increased its dividend for 19 consecutive years, which means that the company has enough ability to resist the economic downturn and even recession, as we have seen during the epidemic. In the past five years, its average dividend has increased by more than 10%.

Nike's payout ratio is only slightly lower than 30%, coupled with the current profit momentum, it is clear that it has a greater ability to increase the payout.